Taxing Times Ahead

Another Budget has come and gone, and speculation over changes to pensions tax relief again proved unfounded – for now. But with the UK’s tax burden set to rise to its highest level since the 1960s (Office for Budget Responsibility, March 2021), the direction of travel on taxation is clear, as the chancellor seeks to repair the nation’s finances.

For those planning their retirement, the removal of some uncertainty will be welcome; but the threat of a less attractive tax regime for pension savers has not gone away. The publication of the government’s tax consultations, to follow up the Budget, may provide more clues to the future direction of taxation on capital and pensions, to name just two.

The chancellor’s decision to freeze Income Tax thresholds and the Capital Gains Tax exemption for the next five years underlines the value of tax shelters such as pensions and ISAs. But which is the best option?

There is little dispute that a pension is the most tax-efficient vehicle available to UK savers. Yet savers were often discouraged because access was restricted. Yet all that changed with the introduction of pension freedoms in 2015, which enabled savers to access their pot freely from the age of 55 onwards. The legislation also allowed individuals to choose who received their pension fund after they’d died.

Unlike pensions, ISAs don’t receive tax relief on contributions; and, of course, active members of workplace pension schemes also benefit from employer contributions of at least 3% of their qualifying earnings. However, the simplicity, accessibility and flexibility of ISAs has made them an incredibly popular savings option since their introduction over 20 years ago. At the end of 2018/19, over £584 billion was held in ISAs (HMRC, Individual Savings Accounts Statistics (ISA), June 2020).

A Question of Balance

The choice of whether to save into a pension or ISA is rarely a binary one. A flexible and tax-efficient retirement plan will normally involve a combination of savings vehicles, which could include other investment types as well. But it’s not straightforward to create the optimum mix to ensure the appropriate use of available tax allowances, and to make sure your retirement income and estate plans are the right ones. That’s where advice can make a huge difference to your future financial wellbeing.

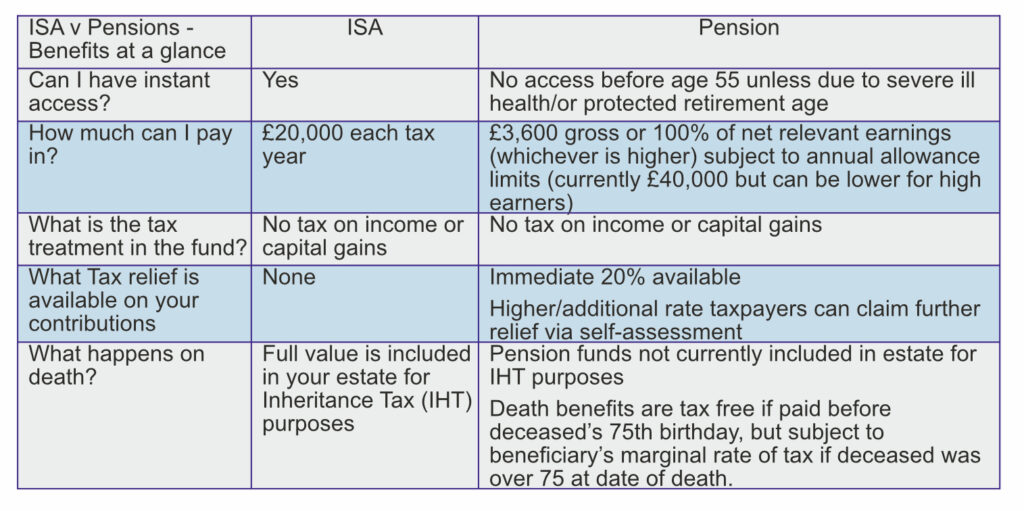

ISA v pensions – benefits at a glance

Using Pension to Reduce Tax and Reclaim Allowances

Another advantage of making personal pension contributions is that it has the effect of reducing your taxable income, which means you can avoid the loss of certain benefits and allowances. Payments into an ISA do not provide the same potential benefits.

For example, if you have a net income of £125,000 or more in this tax year, you will lose all your entitlement to the personal allowance; but by making a net pension contribution of £20,000 (£25,000 including basic rate tax relief), you could bring your taxable income back down to £100,000 and get your whole personal allowance back.

Pension contributions can also help families avoid losing Child Benefit, which is lost if one parent or partner in the household earns more than £50,000. For example, someone earning £52,000 would have to repay 20% of any Child Benefit they receive via self-assessment. But if this individual contributed £2,000 (gross) into a pension, they would be able to retain their full Child Benefit payment and avoid a tax charge.

Options for Income in Retirement

One argument put forward against pensions is that income taken in retirement is potentially taxable, whereas funds from an ISA can be accessed at any time without any tax liability.

The tax savings on income taken from ISAs in retirement can be considerable, as illustrated above, but it’s important to remember that 25% of a pension fund can be taken tax-free and, if available tax allowances are used carefully, income can be taken relatively tax-efficiently.

Additionally, pensioners typically pay lower rates of Income Tax than they did while they were working which means that, in the vast majority of cases, the tax relief gained when putting money into a pension is more than the tax rate on the money taken out.

One other point to consider is whether to prioritise taking income from your ISA savings to leave more of your pension benefits intact, which would enable more of your estate to pass to your beneficiaries tax free. Investing money in an ISA is a smart way to reduce the tax you pay when taking an income in retirement. Let’s say you are retired and over the course of your working life you have built up an ISA pot worth £200,000. If you take 4% of the amount as income each year, that’s £48,000 a year of income that you don’t pay tax on. For higher-rate taxpayers, had that income not been from an ISA, it could have meant paying £3,200 a year in tax (based on 40% marginal rate) or £80,000 over a 25-year retirement.

Act Now

The Budget sent a clear message that effective tax planning will become even more important in the years, and decades, to come. That will need individuals to make the most of all opportunities to reduce their tax bill, and families to pool their resources together to get the maximum value out of their wealth.

To receive a complimentary guide covering wealth management, retirement planning or Inheritance Tax planning, contact Narwal Wealth Management Ltd on 0116 242 67 77 or email narwalwealthmanagement@sjpp.co.uk

The levels and bases of taxation, and reliefs from taxation, can change at any time and are generally dependent on individual circumstances.