How to Ensure You Don’t Leave Your Family with an Avoidable Tax Bill

Taking the right steps now can shield your loved ones from tax and help ensure your money goes where you want it to go after you die.

In the last tax year (2019/20), bereaved families paid some £5.2 billion in Inheritance Tax (IHT) HMRC, Inheritance Tax Statistics 2017-18, July 2020.

However, while many people are aware of strategies that can reduce their IHT liability, such as gifting, they may be less aware of how some employee perks – including workplace pensions and death-in-service benefits (whereby a nominated beneficiary receives a lump sum if you die while in service with your employer) – could be storing up problems for their families in the future.

Death-in-service benefits or pensions that are paid as a lump sum to a beneficiary after the death of the benefit holder will form part of that beneficiary’s estate – and IHT may become payable.

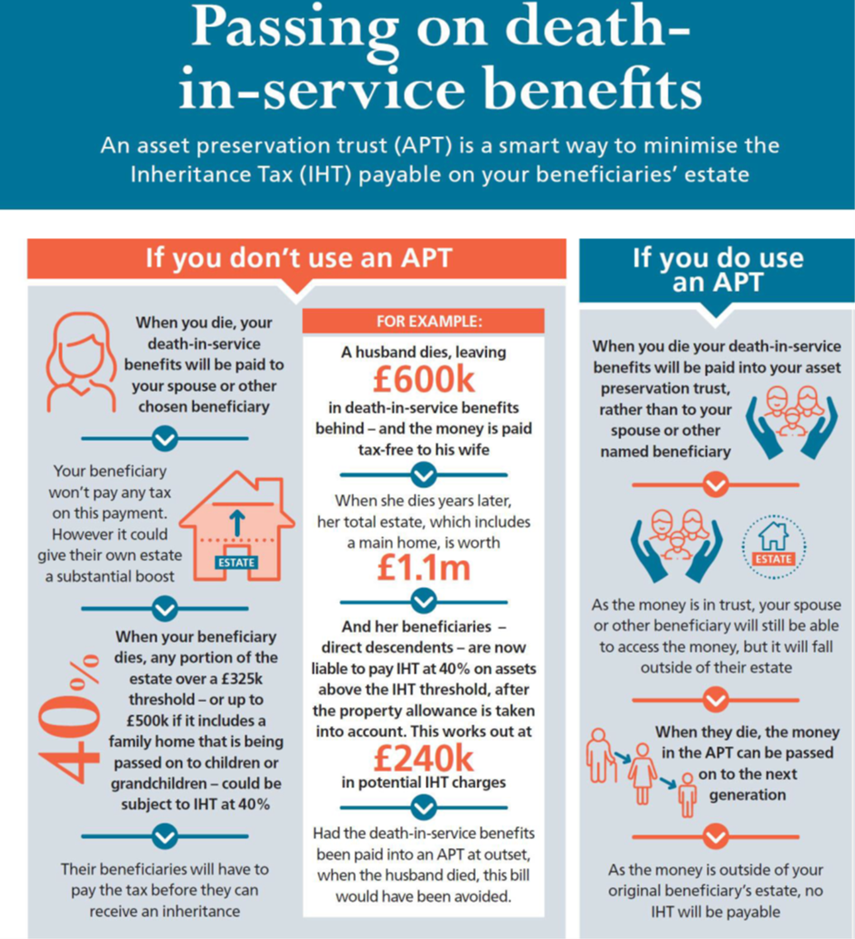

Currently, IHT is charged at a rate of 40% on the portion of the estate over a £325,000 threshold, or up to £500,000 if it includes a family home that is being passed on to children or grandchildren. However, transfers between spouses and civil partners are tax-free.

Death-in-service benefits are often multiples of salary, so even for those who don’t currently have any issues with IHT, a payment from one of these schemes can be as much as, if not more than, the nil rate band i.e. the £325,000 threshold.

Preserving your assets

The problem can, however, be avoided with the use of an asset preservation trust (APT). APTs are designed for the purpose of holding death-in-service and pension death benefits in such a way as to have the funds accessible to your beneficiaries while keeping them outside their estate for IHT purposes. By paying the lump sum into the APT on death, it will avoid it falling into the surviving beneficiary’s estate and so being subject to IHT, while giving the beneficiary access to the capital should they still need it.

The trust can be set up easily by your financial adviser, but you will also have to appoint two trustees who will be responsible for the distribution of your money after you have died. You will also need to inform your employer of your arrangements with an ‘expression of wishes’ form. This will ensure that money is paid into the APT rather than to the estate.

Greater control

The benefits of an APT go far beyond IHT mitigation and need not be the preserve of wealthier families.

If, for example, you have children from a previous relationship/marriage and are worried about what will happen to your wealth if one of your beneficiaries’ divorces, or you are concerned about their ability to manage their finances, an APT provides more control over how and when your money is distributed, and to whom. Money can otherwise quickly drift into other families.

Holding money in an APT can also be helpful if your beneficiary needs care later in life. As the funds in the APT are held outside their estate, they won’t affect eligibility for any means-tested local authority care.

Holding money in an APT can also be helpful if your beneficiary needs care later in life. As the funds in the APT are held outside their estate, they won’t affect eligibility for any means-tested local authority care.

With an APT, the distribution of your estate is controlled by your chosen trustees, who will make decisions based on your instructions. This is why it’s important to have a letter of wishes, which you keep updated, that can be used to drive trustees’ decisions.

Reviews would be recommended following events such as marriage, divorce or the birth of grandchildren. Think about it every time there is a change within the family and consider who you want to benefit.

Getting set up

As a form of discretionary trust, an ATP may be subject to certain tax charges – but these can often be offset by the benefits.

Your Financial Advisor will also be able to advise you if the trust becomes unnecessary – for example, when you have retired and death-in-service benefits are no longer relevant, or when your tax position has changed.

People sometimes think setting up a trust is a hassle, but the merits can outweigh the chores of paperwork and choosing trustees. Think of it as a back-up plan. Often you don’t appreciate why you need one until the time comes. It can be very good in complex family situations because it allows a trustee – whom you trust – to make the decisions for you.

To receive a complimentary guide covering Wealth Management, Inheritance Tax Planning or Retirement Planning, contact Narwal Wealth Management Ltd on 0116 242 67 77 or email narwalwealthmanagement@sjpp.co.uk

Trusts are not regulated by the Financial Conduct Authority.